Back to BlogCorporate Gift Selection

Why Your £133-Per-Person Corporate Gift Budget Damages Both Client and Employee Relationships

25 February 2026

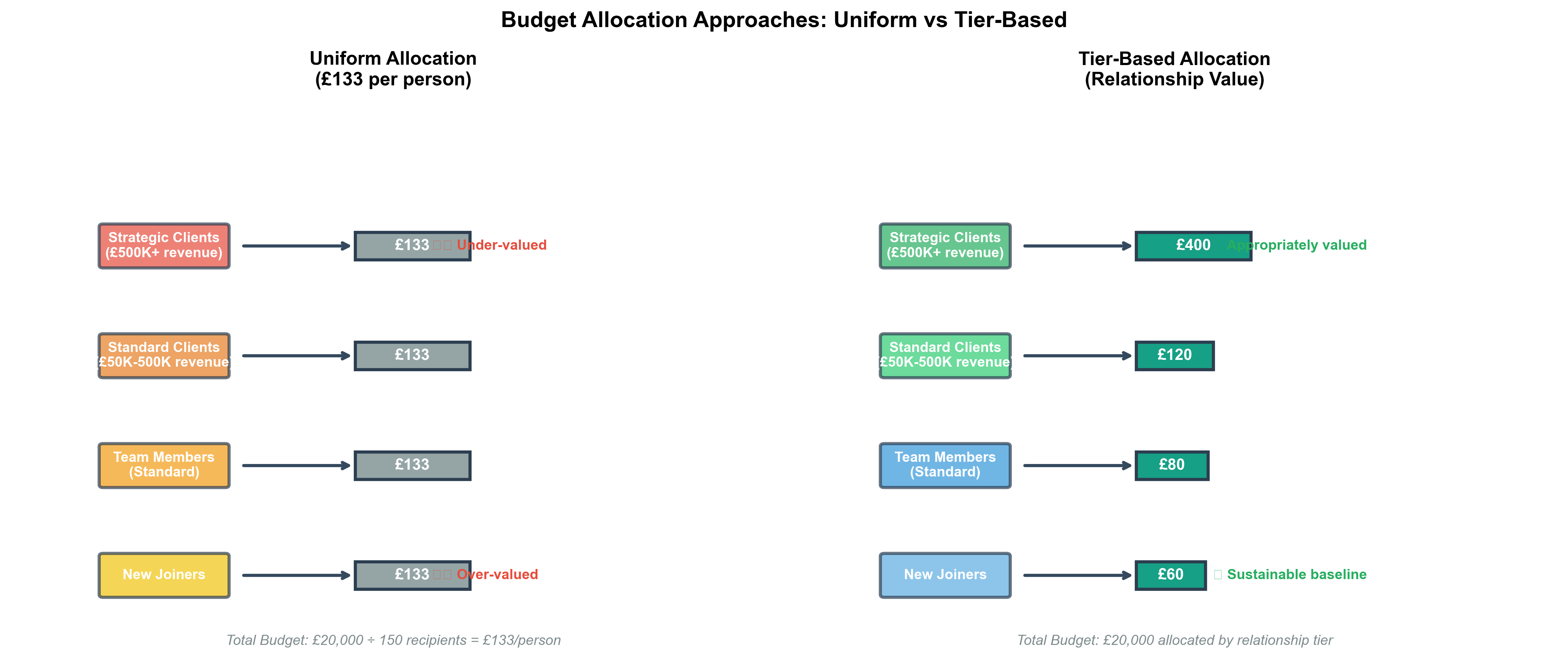

When procurement teams allocate a £20,000 annual corporate gifting budget across 100 employees and 50 clients by dividing the total by headcount, they create a £133-per-person uniform allocation that systematically damages relationships at both ends of the recipient spectrum. This decision pattern—treating corporate gifting as a headcount exercise rather than a relationship value exercise—is one of the most persistent misjudgments we encounter in UK enterprise procurement, and it stems from applying cost-control frameworks that work for office supplies to a function that operates on entirely different economics.

The structural problem begins with how budgets are justified. Finance teams approve gifting budgets based on per-capita metrics because that's how they evaluate every other procurement category. A £20,000 request supported by "£133 per stakeholder across 150 recipients" passes budget approval processes far more easily than a request that segments £50 for junior staff, £100 for mid-tier clients, and £400 for strategic accounts. The uniform allocation creates the appearance of fairness and control, which satisfies internal governance requirements. What it doesn't do is create appropriate relationship signals for the recipients, and that's where the systematic failure begins.

[IMAGE:/images/blog/gift-selection-budget-allocation-comparison.png|Comparison of uniform budget allocation versus tier-based allocation approaches for corporate gifting]

At the lower end of the recipient spectrum, uniform allocation creates expectation inflation that becomes operationally expensive to sustain. When a new graduate joiner receives a £133 welcome kit on their first day—perhaps containing a premium notebook, branded water bottle, and high-quality pen set—they internalise that as the company's standard expression of appreciation. Six months later, when they receive a £133 birthday gift, and twelve months later when they receive a £133 work anniversary gift, the company has established a £400-per-year gifting baseline for that employee. Multiply that across cohorts, and the procurement team discovers they've committed to a recurring cost structure that wasn't intended. More critically, because the initial gift set expectations at a premium level, any subsequent reduction in gift value—say, dropping to £50 for routine occasions—is perceived as a downgrade in how the company values that employee. The uniform allocation has created a ratchet effect where the baseline can only move upward.

At the upper end of the recipient spectrum, the same £133 allocation creates a perception gap that's nearly impossible to recover from in subsequent business interactions. When a client who has just signed a £500,000 annual contract receives a corporate gift box valued at £133—roughly equivalent to what their company spends on client lunches—the gift communicates that the supplier views this £500K relationship as interchangeable with every other stakeholder relationship. The client doesn't necessarily know the exact cost of the gift, but they recognise the category: mid-range corporate merchandise, the kind distributed at industry conferences. For a relationship at this revenue scale, the appropriate gift tier in UK B2B contexts typically ranges from £300-500, incorporating bespoke elements that signal the relationship is valued distinctly. The £133 uniform allocation has positioned the supplier as transactional rather than strategic, and that perception influences how the client approaches contract renewals and competitive bids.

[IMAGE:/images/blog/gift-selection-perception-gap.png|How uniform budget allocation creates perception gaps for strategic clients and new employees]

The misjudgment becomes particularly visible when companies attempt to correct course mid-year. A procurement manager realises that the £133 allocation is under-serving VIP clients and proposes reallocating budget to create a £400 tier for the top 20 accounts. This immediately surfaces the structural problem: if you move £5,400 from the general pool to the VIP tier (20 clients × £267 increase), the remaining 130 recipients now receive £112 each instead of £133. The company is now in the position of either reducing gift value for existing recipients—which creates visible dissatisfaction—or requesting additional budget, which requires re-justifying the entire gifting programme to finance. The uniform allocation has created a locked-in cost structure that resists optimisation.

In practice, this is often where corporate gift selection decisions start to be misjudged. Procurement teams focus on unit cost control and budget utilisation rates, applying the same frameworks they use for managing stationery or IT equipment purchases. But corporate gifting operates on relationship economics, not unit economics. The value of a gift is not its cost; it's the signal it sends about how the relationship is categorised. A £133 gift to a graduate joiner signals "we value you as a new team member." The same £133 gift to a £500K client signals "we categorise you the same way we categorise everyone else." Both messages are clear, but only one is appropriate.

The companies that avoid this failure don't start with a total budget and divide by headcount. They start by defining relationship tiers based on strategic value—typically three to four tiers for employees (new joiners, standard team members, senior contributors, leadership) and three to four tiers for clients (prospects, standard accounts, growth accounts, strategic partnerships). Budget allocation follows tier definition, not headcount. A company might allocate 60% of the gifting budget to the top 15% of recipients by relationship value, 30% to the middle 50%, and 10% to the remaining 35%. This creates appropriate differentiation in gift value: £400 for strategic accounts, £120 for standard clients, £60 for prospects. The total budget is the same, but the relationship signals are now aligned with business priorities.

The operational challenge is that tier-based allocation requires procurement teams to make explicit judgments about relationship value, which introduces subjectivity that finance teams resist. It's easier to defend a uniform £133 allocation in a budget review than to defend why Client A receives £400 while Client B receives £120. But this is precisely the judgment that procurement should be making. [Selecting appropriate corporate gifts for different business contexts](https://britgift.works/resources/corporate-gift-selection-guide) requires understanding that the decision framework is strategic, not administrative. The role of procurement in corporate gifting is not to achieve cost parity across recipients; it's to ensure that gift value aligns with relationship value in a way that reinforces business objectives.

When uniform budget allocation creates systematic relationship damage at both ends of the recipient spectrum, the financial cost is often invisible in the short term. The £133 gift to the £500K client doesn't immediately trigger contract cancellation. The £133 welcome kit to the new joiner doesn't immediately create retention problems. But over 12-24 months, the cumulative effect becomes measurable. Client satisfaction scores decline in the "valued partner" category. Employee engagement surveys show lower scores in "company appreciation" metrics. Competitors who have implemented tier-based gifting strategies are winning renewals and attracting talent, and the procurement team is left trying to explain why their "fair and consistent" gifting programme is producing worse outcomes than approaches that explicitly create differentiation.

The correction path requires recognising that corporate gifting is not a cost centre to be optimised through unit cost control. It's a relationship investment where the return is measured in retention rates, contract renewals, and brand perception. Uniform budget allocation optimises for internal governance simplicity at the expense of external relationship effectiveness. Tier-based allocation optimises for relationship outcomes at the expense of internal administrative complexity. The choice between these approaches is a choice about whether procurement's primary accountability is to finance processes or to business outcomes, and that choice determines whether corporate gift selection functions as a strategic tool or an administrative checkbox.

You May Also Like

Rigid Box vs. Corrugated Mailer: Which Material Suits Your Premium Corporate Gifts?

A deep dive into the structural integrity, cost implications, and unboxing experience of rigid boxes versus corrugated mailers for high-end corporate gifting.

Foil Stamping vs. UV Spot: Elevating Your Brand Logo on Custom Gift Boxes

A technical comparison of hot foil stamping and UV spot varnish, analyzing visual impact, durability, and production costs for branded corporate packaging.